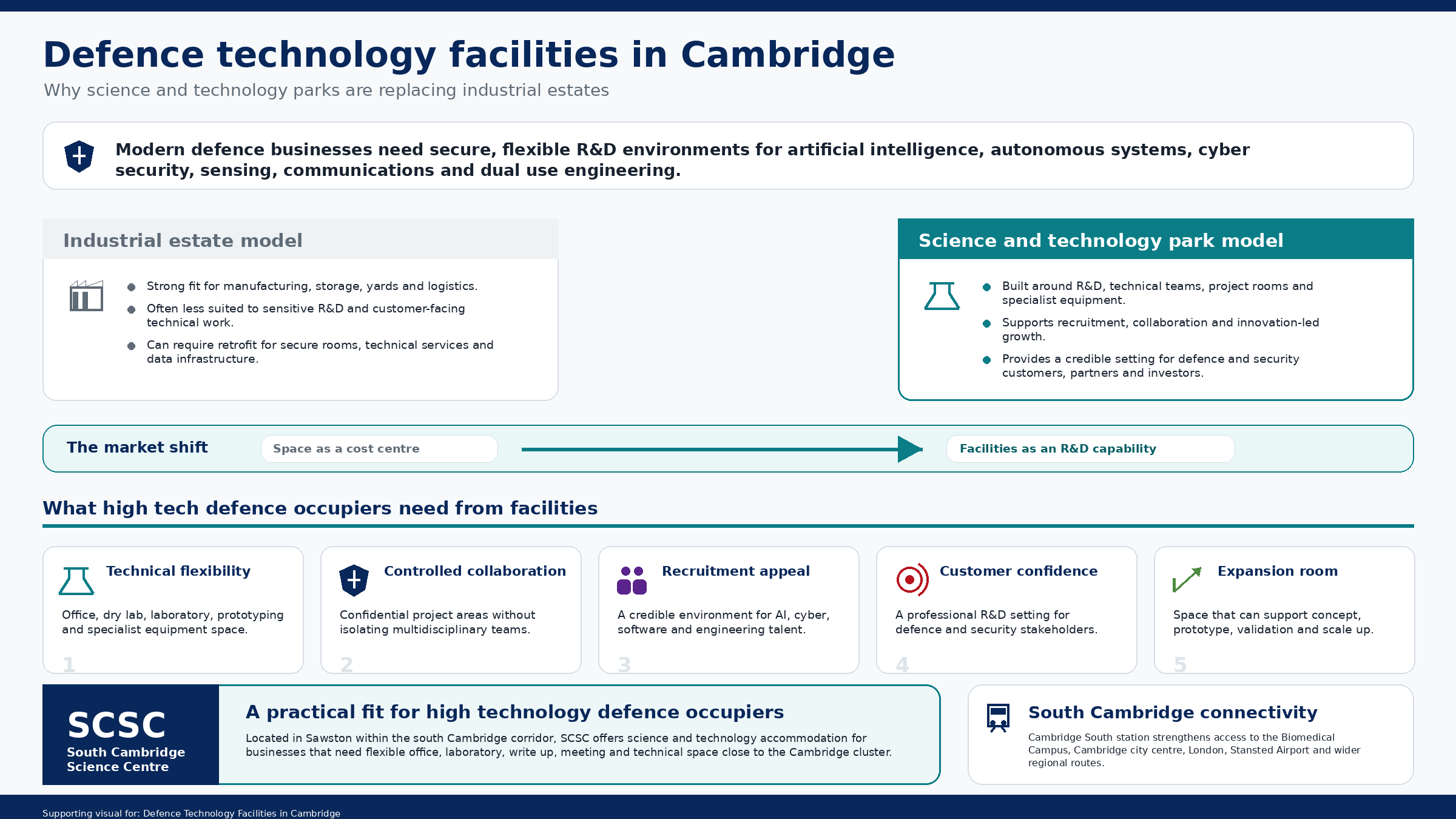

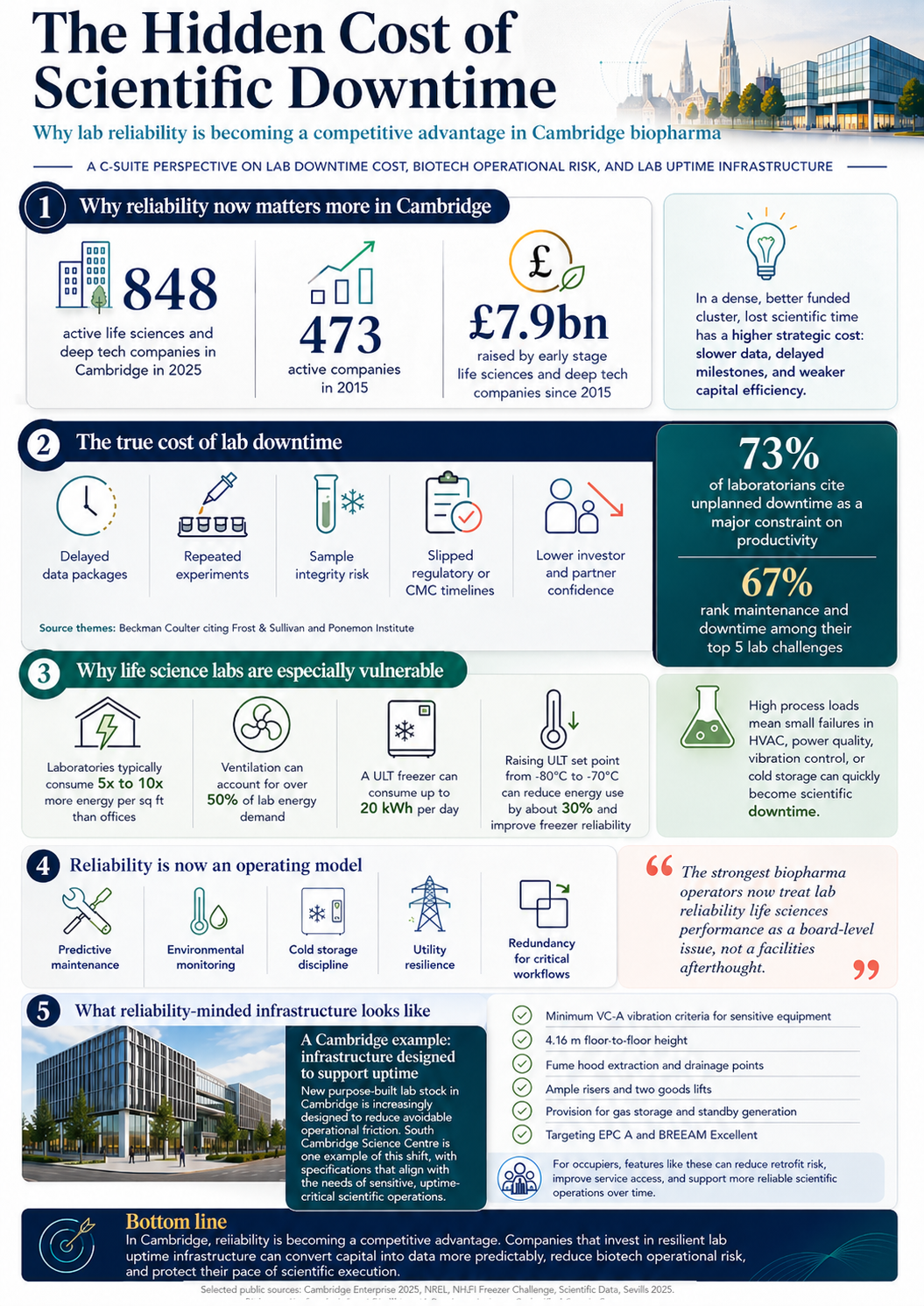

The property requirements of defence companies are changing. For many years, defence accommodation was associated with industrial estates, manufacturing sheds, logistics yards and large operational compounds. Those locations remain important for production, storage, vehicle work and heavy engineering. But the fastest growing parts of the sector increasingly need a different type of environment.

Modern defence businesses are being shaped by artificial intelligence, autonomous systems, cyber security, secure communications, robotics, space technology, advanced sensing, biosecurity and dual use engineering. These companies are not simply searching for square footage. They need high quality research and development space that can support technical teams, sensitive project work, customer engagement and future expansion.

That shift is making science and technology parks more important to the defence property market. It is also making Cambridge a stronger location for the next generation of defence and security companies.

Defence innovation is becoming more technical

The UK defence sector is moving toward faster adoption of advanced technology. Innovation is no longer confined to established defence primes or conventional suppliers. It increasingly involves specialist SMEs, university linked companies, cyber firms, AI businesses, engineering consultancies and dual use technology companies serving both commercial and defence markets.

This has changed what defence occupiers need from buildings. A company developing autonomous navigation, secure communications, cyber defence software, sensor fusion, battlefield data tools or AI enabled decision support may not require a traditional industrial estate as its first growth location. It may need secure R&D space in Cambridge, with office, laboratory, engineering and collaboration areas in one integrated setting.

For these occupiers, a facility is part of the operating model. The building must help the company recruit technical talent, protect sensitive work, host customers, support product development and scale as programmes mature. A location that only solves the immediate space requirement may become a constraint once the company moves from concept to prototype, demonstration and deployment.

Why industrial estates often fall short

Industrial estates are usually designed around practicality and cost. They can provide loading access, yard space, manufacturing areas and storage. For some defence uses, that remains appropriate. But for high value defence technology, the requirement is more complex.

A growing defence company may need dry labs, electronics benches, secure project rooms, resilient power, specialist data infrastructure, clean office space, prototype areas, meeting rooms and flexible areas that can change as programmes develop. It may also need an environment that appeals to software engineers, physicists, systems architects, cyber specialists and commercial teams.

Those needs are difficult to satisfy in many generic industrial locations. Retrofitting specialist infrastructure can be expensive. Poor amenities can make recruitment harder. Limited flexibility can force relocation at exactly the point when a company should be focused on delivery. A low headline rent can become less attractive once fit out, downtime, utilities, staff travel and future expansion are considered.

Science and technology parks are better aligned with this operating model. They are designed for organisations whose value is created through research, technical talent, intellectual property and innovation. They also provide a more credible setting for customer meetings, investor visits, grant funded projects and collaboration with universities, partners or public sector bodies.

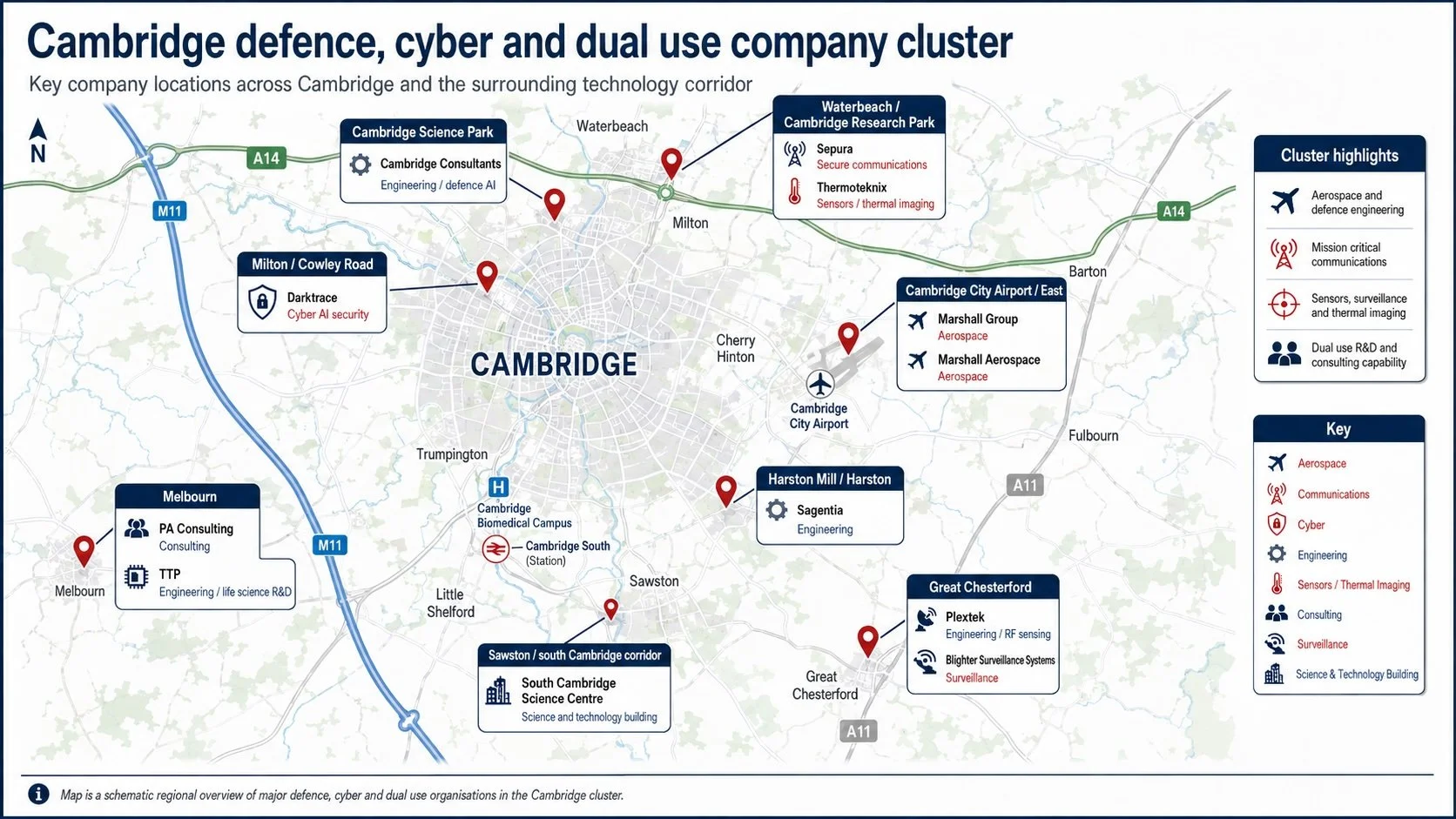

Cambridge is well placed for defence technology

Cambridge is not a traditional defence manufacturing city. Its strength lies in deep technology, software, engineering, life sciences, communications, sensing, cyber security and applied research. That makes it highly relevant to the future of defence.

This is why searches for defence technology Cambridge and defence innovation Cambridge increasingly point toward businesses that operate across sectors. The relevant market includes cyber security companies, autonomous systems developers, engineering consultancies, medtech specialists, AI businesses, diagnostics companies and advanced hardware developers.

This broader cluster is important. Defence companies Cambridge should not be understood only as traditional military suppliers. The next generation of defence capability is more likely to come from companies working across cyber, data, sensing, communications, resilience, human performance and dual use science.

For these companies, location matters. They need access to technical people, academic networks, engineering knowledge, commercial partners and transport links. They also need buildings that can accommodate a mix of office, laboratory, write up, project and technical space.

What high tech defence occupiers need from facilities

The strongest locations for defence technology companies share several characteristics.

They provide technical flexibility. Defence companies working across software, hardware, sensors, data, communications and engineering need buildings that can adapt. A company may begin with office and dry lab space, then add testing, prototyping, secure project areas or specialist equipment.

They support controlled collaboration. Defence and security work often requires confidentiality, restricted areas and careful visitor management. But teams still need to work across disciplines. A good building allows separation where necessary without fragmenting the company.

They support recruitment. The best technical people have choices across AI, cyber, life sciences, robotics, medtech and advanced engineering. A credible science and technology environment helps make a company more attractive to the people it needs to hire.

They support customer confidence. Defence and public sector customers expect professionalism, reliability and operational discipline. A high quality R&D environment strengthens that impression.

They support expansion. Defence technology companies often grow in stages: concept, prototype, demonstration, customer validation and scale up. A building that only satisfies the first stage can become a constraint at exactly the wrong moment.

South Cambridge Science Centre and the defence property opportunity

South Cambridge Science Centre fits this changing market because it provides science and technology accommodation in a location that gives occupiers access to the Cambridge cluster without forcing them into the most constrained central areas.

The centre is in Sawston, within the south Cambridge corridor. This is an important distinction. South Cambridge Science Centre is not positioned as a traditional defence estate. Its opportunity is different. It offers a modern science and technology setting for companies whose defence relevance comes from advanced R&D, data, engineering, cyber security, sensing, communications, biosecurity or dual use technology.

For a defence technology company, that matters. Cyber, sensing, communications, autonomy, biosecurity and engineering businesses may each need a different mix of office, laboratory, write up, meeting and technical space. Flexibility is not a convenience. It is part of the operational requirement.

South Cambridge Science Centre also sits within a strengthening south Cambridge geography. Cambridge South station provides direct rail access to the Cambridge Biomedical Campus and improves connectivity between the southern cluster, Cambridge city centre and wider regional transport routes. For defence occupiers, that connectivity matters. Public sector customers, strategic partners, technical advisers, investors and senior recruits need to reach the site efficiently.

Location is not simply a map point. It affects how easily a company can work with the wider market.

A practical alternative to conventional defence property

The defence market is becoming more digital, more scientific and more closely linked to dual use technology. Industrial estates remain useful for manufacturing and logistics, but many defence technology companies now need facilities that look more like high specification R&D environments. They need buildings where research, product development, secure collaboration and technical growth can happen together.

South Cambridge Science Centre answers that brief in a way that a conventional industrial estate often cannot. It gives occupiers access to the Cambridge science and technology cluster, while offering the type of flexible accommodation needed by companies working in artificial intelligence, autonomous systems, cyber security, sensing, communications and other advanced defence applications.

For defence companies looking for property in Cambridge, the strongest locations will combine technical capacity, flexibility, transport access, talent proximity and room to grow. South Cambridge Science Centre offers a compelling south Cambridge base for companies that need more than industrial space. It provides a practical setting for defence innovation in one of the UK’s most important science and technology clusters.