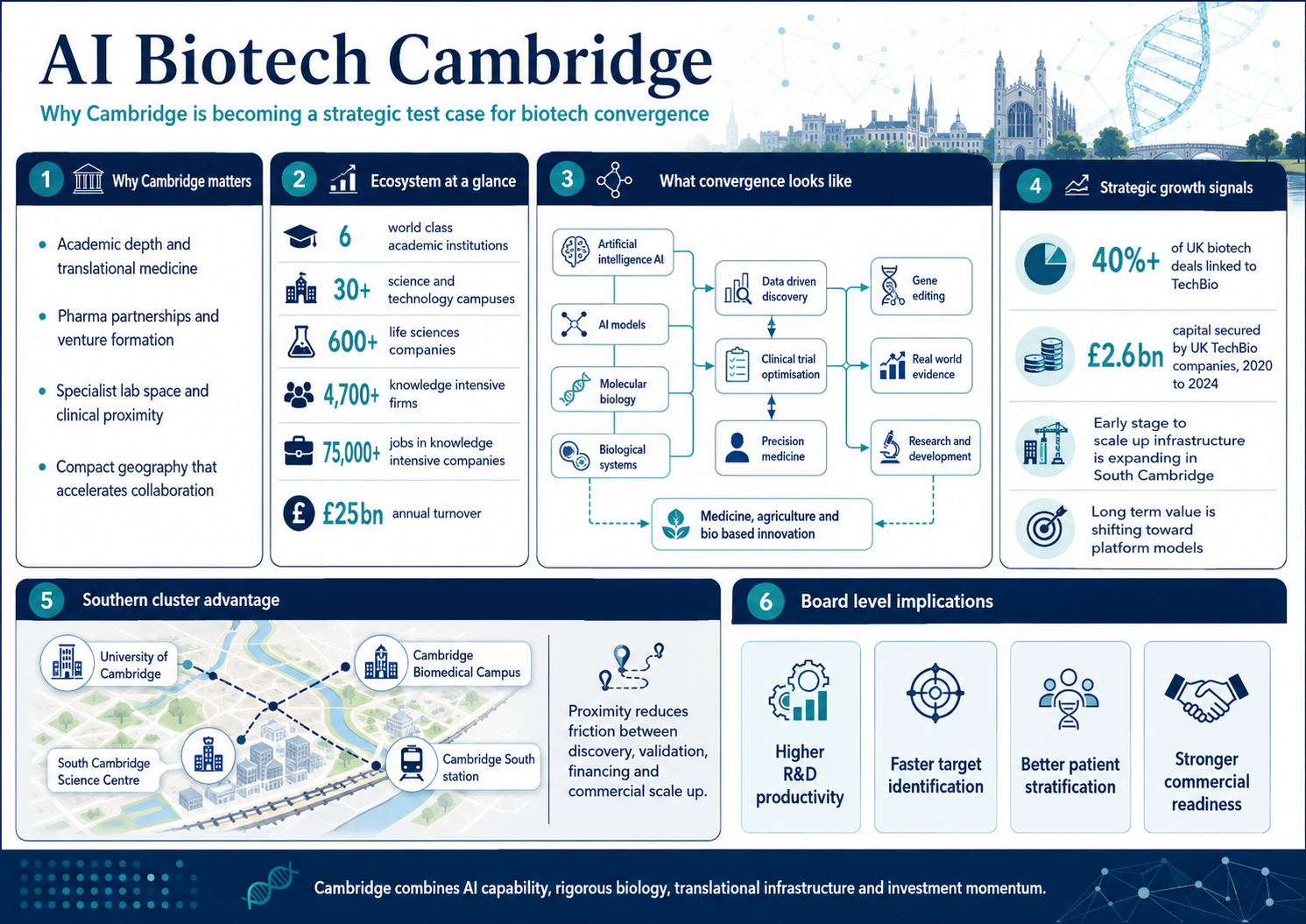

Cambridge has moved beyond its historic position as a strong life sciences cluster. It is now becoming a strategic test case for the convergence of artificial intelligence AI, biotechnology and translational research. For C suite leaders, the importance is not only scientific. It is commercial, operational and competitive.

The city combines academic depth, pharma partnerships, clinical proximity, venture formation, specialist real estate and research and development capability in a compact geography. That combination is increasingly valuable as biotech technology trends move from wet lab discovery alone toward computational biology, molecular biology, multimodal data, automated experimental design and AI models that can interrogate complex biological systems.

The UK Government’s Life Sciences Sector Plan, published in 2025, sets a national ambition for the UK to become Europe’s leading life sciences economy by 2030 and the third globally by 2035. The plan also identifies TechBio, the fusion of biotechnology with data science, as a priority growth area and commits more than £2 billion of government funding over the Spending Review period alongside UKRI and NIHR support.

Cambridge is unusually well positioned to capture that agenda. Cambridge University Health Partners describes the local ecosystem as including six world class academic institutions, more than 30 science and technology campuses and more than 600 life sciences companies including AstraZeneca, GSK, Abcam and Illumina. The University of Cambridge’s 2025 innovation data reports more than 4,700 knowledge intensive firms, more than 75,000 people employed by those firms and £25 billion in annual turnover generated by knowledge intensive companies in the Cambridge city region.

The rise of AI biotech Cambridge is therefore not an isolated technology story. It is the next phase of a cluster model that already has scale, density and institutional connectivity. CBRE’s 2025 Cambridge market profile describes the city as one of Europe’s most advanced life sciences hubs, with end-to-end capability from discovery to translation and commercialisation. It also notes that life sciences activity is concentrated mainly in the southern cluster while technology is more prevalent in the north and city centre. That geography matters because convergence depends on proximity between data science, biology, clinical assets, capital and specialist infrastructure.

For executives, the first board level implication is productivity. Traditional drug discovery remains expensive, slow and exposed to high attrition. AI does not remove biological risk, but it can improve target identification, molecule design, patient stratification, clinical trial prioritisation and real-world evidence generation. The strategic value is not simply speed. It is the ability to make better decisions earlier, reduce unproductive programmes and strengthen the evidence base behind precision medicine.

The capital market already reflects that shift. The UK BioIndustry Association reported in 2025 that TechBio, defined as the combination of data, AI and biotechnology, has moved into the mainstream and accounted for more than 40 percent of UK biotech deals in recent years. It also reported more than £2.6 billion of capital secured by UK TechBio companies between 2020 and 2024.

Major transactions reinforce the point. The BIA highlighted the £489.6 million acquisition of Exscientia by Recursion as evidence that UK science is creating global value through TechBio. More recently, Isomorphic Labs has attracted substantial funding momentum for its AI powered drug discovery work, with recent reporting putting its latest raise at $2.1 billion. For boards assessing AI drug discovery UK strategy, these are not speculative signals. They show that investors are underwriting platform models and data driven discovery engines, not only single therapeutic assets.

Cambridge is already producing relevant company formation. CardiaTec Biosciences, a University of Cambridge linked company, uses AI to identify new cardiovascular treatments. Cambridge Enterprise states that CardiaTec integrates genetics, gene expression, epigenetics and proteomics to understand disease mechanisms. Its work shows how Cambridge biotech innovation is increasingly interdisciplinary by design, combining computational capability with molecular biology and disease specific knowledge.

The city’s translational infrastructure is equally important. The Milner Therapeutics Institute’s Bio Incubator offers access to serviced laboratory equipment and potential interaction with clinicians, researchers and drug discovery scientists on the Cambridge Biomedical Campus. For early-stage Cambridge science companies, that can reduce the friction between academic discovery, validation, pharma engagement and investor readiness.

South Cambridge Science Centre should be viewed in that context. Its importance is not only real estate provision. It is an ecosystem development story. SCSC is emerging as an affordable platform for early stage and scale up companies that need wet lab capability, dry lab flexibility, commercial proximity and cost discipline. That specification fits the hybrid operating model now common in AI enabled biotechnology, where computational teams, biology teams, automation workflows and translational science must operate in close sequence rather than in separate silos.

A key validation point is the arrival of Frontier IP Group plc, the intellectual property commercialisation specialist. In June 2025, Frontier IP announced a strategic partnership with Abstract Mid Tech Limited to create an innovation hub at South Cambridge Science Centre. Under the agreement, Frontier IP is taking a 20 year lease on approximately 18,000 sq ft at SCSC and intends to sublet space to portfolio companies and other innovative companies aligned with its focus on deep technology and life sciences.

For C suite leaders and investors evaluating Cambridge biotech innovation, the strategic importance is clear. It is bringing a commercialisation engine into the building. That creates a more useful operating environment for founders than conventional accommodation alone. Early-stage occupiers should benefit from closer access to commercialisation expertise, investor engagement, corporate partner visibility and peer company interaction.

The wider market has recognised the transaction. Savills identified Frontier’s 18,000 sq ft commitment at South Cambridge Science Centre as the largest laboratory letting in Cambridge during the first half of 2025 and noted that the space will provide incubation capacity for Frontier’s portfolio companies. That matters because it demonstrates institutional demand for high specification space in the southern Cambridge cluster and shows that SCSC is being adopted by organisations with a direct interest in deep tech and life sciences company creation.

The surrounding ecosystem strengthens the proposition. SCSC is located in Sawston, south of Cambridge and close to the Cambridge Biomedical Campus, the University of Cambridge and emerging transport infrastructure around Cambridge South station. Network Rail says Cambridge South station is expected to open to the public on 28 June 2026 and will provide connectivity to the biomedical campus and the wider region. For occupiers, that matters because talent acquisition, clinical collaboration and investor access are affected by transport efficiency as much as by laboratory specification.

This is why SCSC is a positive addition to the AI biotech Cambridge landscape. The convergence of AI and biotechnology does not happen through software capability alone. It requires physical infrastructure, repeatable experimental validation and a community of companies moving through similar technical and commercial inflection points. With Frontier IP’s innovation hub embedded in the centre, SCSC has the potential to operate as a concentration point for the next generation of AI drug discovery UK, diagnostics, engineering biology, gene editing and platform technology companies.

The strategic opportunity extends beyond medicine. The same convergence logic will influence medicine agriculture and bio-based manufacturing, where biological systems, automation and AI models can support new approaches to materials, food production, crop resilience and industrial biotechnology. Cambridge’s advantage is that its research base can support both therapeutic innovation and broader bioeconomy applications without treating them as disconnected markets.

The competitive picture still requires discipline. The challenges including biological validation, data quality, regulatory confidence, reimbursement, talent access and capital intensity remain substantial. A weak AI model can create false confidence. Poor experimental design can waste capital. A company without proprietary data, clinical relevance or credible translation pathways can look technically sophisticated while remaining commercially fragile.

The AstraZeneca investment story shows why this matters at board level. In September 2025, AstraZeneca paused a planned £200 million Cambridge expansion, which was widely interpreted as a warning signal for UK pharmaceutical competitiveness. More recent reporting says the company has since revived UK investment plans, including Cambridge, as part of a £300 million package. The lesson is not that Cambridge is fragile. The lesson is that innovation clusters win over the long term only when science, infrastructure, market access, capital and policy remain aligned.

Competition from the United States remains relevant. US capital depth, large pharma demand, reimbursement scale and specialist AI infrastructure continue to influence where companies build, finance and commercialise. Cambridge’s response should not be to imitate the United States, but to convert its own advantages into operating leverage: strong biology, clinical adjacency, trusted data access, founder support, specialist real estate and translational speed.

The executive conclusion is clear. Cambridge’s advantage in AI and biotech convergence is structural, not cosmetic. The city combines research excellence, clinical proximity, specialised infrastructure, pharma connectivity and a growing TechBio investment market. The opportunity for boards is to treat Cambridge not only as a location choice, but as an operating system for accelerated discovery and translation.

The companies that benefit most will be those that pair AI capability with rigorous biology, secure proprietary data, credible clinical pathways and disciplined capital allocation. In that context, Cambridge and assets such as South Cambridge Science Centre are well placed to support the next cycle of biotech technology trends, from AI assisted discovery and data rich translational medicine to precision medicine and commercially scalable platform biology.